JPMorgan scoops best-performing accolade among largest US banks

The Banker’s inaugural best-performing banks ranking, from the The Banker Database, assesses the 10 largest US lenders for their strength in categories such as asset quality, liquidity and efficiency. While JPMorgan leading the way is no surprise, other banks also impress, as Silvia Pavoni reports.

Never is resilience more important than in a time of crisis. In this regard, The Banker’s new rankings measuring US banks’ asset quality, liquidity and operational efficiency, among other performance indicators, could not be more timely.

As the coronavirus pandemic continues to spread across the world, affecting people’s health and livelihoods as well as the economy, banks of all sizes will be tested. Our new US ranking examines a number of factors to better understand banks’ strength and profitability. It examines the US’s 10 largest names by Tier 1 capital, in keeping with The Banker’s traditional ranking, and combines various indicators to assess overall performance as well as performance in specific areas.

The US’s largest bank by Tier 1 capital, JPMorgan, also tops the overall performance ranking. Several factors explain how the bank achieved this position. It is the best performing for liquidity, as expressed by the combination of its loans-to-assets ratio and loans-to-deposits ratio, but which also takes into consideration annual changes.

JPMorgan also leads in the operational efficiency table, which looks at the cost-to-income ratio and its annual change. And it is again in the top spot in the return on risk table – which is based on banks’ return on risk-weighted assets ratios – as well as on the profitability table, which considers return on assets, return on equity, profit margin and asset utilisation ratios. As for all other indicators, those for both return on risk and profitability include annual changes.

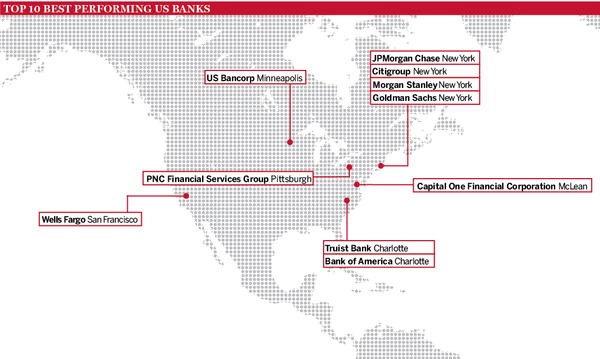

While Bank of America, Wells Fargo, Citigroup and Goldman Sachs follow JPMorgan in terms of Tier 1 capital size, other banks assessed by performance metrics include Capital One Financial Corporation, Morgan Stanley, PNC Financial Service Group, Truist Bank and US Bancorp.

New entity emerges

Asset quality is another helpful indicator of resilience. Truist Bank leads by this measure, which is defined as the combination of the allowance for loan losses on total loans ratio, non-performing loans ratio and the impairment charges to total operating income ratio; as well as by the changes to those values compared with the previous year.

A new entity born at the end of 2019, Truist Bank is the result of the $66bn merger between SunTrust and BB&T and is now the ninth largest bank in the US by Tier 1 capital. The new bank’s ratios are compared with the 2018 figures for BB&T, which technically, as far as banking supervisors are concerned, is the surviving entity to which the additional operations have been added. For this reason, it is not surprising to see Truist Bank lead in the growth table too, where growth is measured as the combination of annual growth in assets, loans, deposits and operating income. In this table, JPMorgan follows Truist Bank by some distance.

Capital One, seventh by Tier 1 capital in the country, leads both the soundness and leverage tables. The former is based on capital asset ratios and their annual change, while the latter looks at total liabilities to total assets ratios and at their variation from the previous year.

While New York remains a leading global financial centre, the US’s 10 largest banks are scattered around the country: four are in New York; two in Charlotte (North Carolina); and one each in McLean (Virginia), Pittsburgh (Pennsylvania), Minneapolis (Minnesota) and San Francisco (California).

Methodology

The Banker’s global and regional rankings are industry-standard measures of bank size by Tier 1 capital. While the current rankings include some additional data to give an overall impression of bank performance, they use only a fraction of the very detailed analysis undertaken by our research team.

Knowing which bank is biggest, or has grown fastest, is useful but what people really want to know is “which bank is the best performer?”.

We have developed a model that scores and ranks banks in eight key performance categories, using 17 ratios, and assigns an overall best-performing bank score and ranking.

The key requirement of the model was that it could be used to identify the best performers in any sample group, be it an existing global, regional or country ranking or custom peer group such as global systemically important banks.

The model only uses performance ratios, and year-on-year percentages and basis points changes, so the size of a bank has no influence on its best bank ranking position.

The performance categories and indicators are:

Growth – Annual percentage growth in assets, loans, deposits and operating income.

Profitability – Return on assets, return on equity, profit margin, asset utilisation (and annual basis points [bps] change in these ratios).

Operational efficiency – Cost-to-income ratio (and annual bps change in these ratios).

Asset quality – Allowance for loan losses to gross total loans, non-performing loans, impairment charges to total operating income (and annual bps change in these ratios).

Return on risk – Return on risk-weighted assets (and annual bps change in this ratio).

Liquidity – Loans-to-assets ratio, loans-to-deposits ratio (and annual bps change in these ratios).

Soundness – Capital assets ratio (and annual bps change in this ratio).

Leverage – Total liabilities to total assets (and annual bps change in this ratio).

When the peer group data is imported, the model assigns a score for each indicator based on the relative distribution of values. Thus a bank that significantly outperforms on a particular indicator will receive a proportionately higher score. The maximum possible score for each category is 10 points and the maximum overall score is 80 points.

The model is neutrally weighted so that the underlying ratios and annual bps changes are of equal significance. Each performance category receives equal weighting. We plan to produce an online version of the benchmarking tool, which will allow users to assign data point and category weights according to their own preferences.